State insurance commissioners and legislators play a critical role in determining the insurance premiums people pay for their home insurance.[1] Insurance companies have increased homeowners insurance premiums by an average of 24 percent from 2021 to 2024 nationwide.[2] Premium rates are rising far faster in many places across the country including in a geographically diverse group of states like Utah (59 percent), Illinois (50 percent), Arizona (48 percent), Pennsylvania (44 percent), and Louisiana (34 percent).[3] Florida homeowners saw the highest absolute cost increase from 2021 to 2024 ($2,118 per policy, equivalent to a 29 percent price hike).

Steeper insurance costs compound housing unaffordability and make it harder for families to make ends meet with the steadily rising cost of living. Rising insurance premiums are responsible for higher credit card debt, higher credit card default rates, and higher mortgage delinquency rates.[4]

Insurance price hikes can be opaque and overwhelming for homeowners—with insurers often providing little explanation and few avenues for recourse. The rate-setting process is complex, largely hidden from public view, and is not always fair. In states that require government approval for insurance rate increases, state insurance commissioners are the decision-makers when it comes to allowing annual price changes requested by insurers, though some commissioners have more authority, capabilities, and inclination to deny steep increases than others.

There is generally a multi-step process for home insurance rate-setting.

- First, insurers establish and submit to the regulators a proposed statewide baseline rate and a set of factors that define how the insurer will adjust that rate for certain groups of customers, properties, or areas based on historical losses.

- Second, in the 15 states that require prior approval by the state, insurance commissioners review and either approve or disapprove the rate increase (in other words, how much bills will go up on average statewide) or ask the insurer to modify its request. In some states, there is an opportunity for homeowners and advocates to engage in the rate approval process. Unfortunately, in 35 states, the District of Columbia and Puerto Rico, insurers are not required to gain approval from the insurance commissioner before increasing rates.[5]

- Finally, insurance companies calculate individual premiums they charge individual homeowners based on the statewide baseline rate and coverage amount for the specific policy, combined with factors specific to the property and policyholder.

All states should strengthen their regulatory oversight over property insurance rate-setting and calculation of premiums to prevent insurance companies from imposing unfair or discriminatory price hikes on families. To do so, states should pass laws to require prior approval of insurers’ rate filings by the insurance commissioner and provide meaningful public participation for people and advocates. Even insurance commissioners with the ability to negotiate and approve rate increases do not always diligently exercise this authority. Insurance commissioners should use all tools available to them to cut down on unfair or discriminatory pricing.

Insurance pricing reflects risk, profits, and unfair socioeconomic factors

Insurers set proposed baseline rates for home insurance premiums primarily on underwriting, actuarial, and business factors.[6] Underwriting and actuarial factors reflect the likelihood and potential cost of reimbursing homeowners for losses from natural disaster, fire, theft, or other risks covered by the policies. Factors include historical claims paid to policyholders, number of policies, property values, changes to property risk from climate change and local conditions, and other risks. Additional business factors that insurers consider include expected expenses (such as salaries, taxes, and the costs of reinsurance),[7] reserve requirements, and targeted underwriting profit margins. Insurers must also submit supporting documentation to justify why they need higher baseline rates to cover growing risks and costs.

Many state laws require that rates be “justifiable,” “reasonable,” and/or not “arbitrarily inflated,” “excessive,” or “discriminatory.”[8] But there are no uniform standards for these considerations or what constitutes ‘reasonable’ profits, and profit margins vary considerably between states and across years.

Once a rate is in effect, insurers use that rate as the baseline to calculate individual premiums, adjusted by the approved factors that are individual to the property or policyholder, including the age and condition of the home, the local perils, and the chances of disasters striking as climate change worsens, among other factors.

Want to check your insurer’s math? You can’t.

For homeowners who want to fully understand how their premiums are calculated, one challenge is that insurers do not usually file their full “rate manual” that includes the full list of factors they consider in setting premiums. Typically, companies only include the handful of factors that they are adjusting in a particular rate filing to an insurance commissioner. To uncover the full set of factors that affect their premiums, consumers would need to piece together many years or decades of rate filings by their insurer, a difficult or potentially impossible task.

Unfortunately, homeowners’ specific premiums are not calculated wholly—or sometimes even primarily—based on property-level risk. While insurers do include risk-based factors in their premium calculations, they often fail to take into account property, community, or landscape scale resilience factors,[9] and also unfairly include socioeconomic factors unrelated to risk. In all but three states, insurers use factors like credit scores—which are unconnected from the disaster risk for a property[10]—that disproportionately penalize lower-income and Black, Latine, and Indigenous policyholders.[11] This extends the long history of racial discrimination that the insurance industry has justified on socioeconomic grounds that continues to this day.

The property insurance industry has long failed to fairly serve families and communities of color, a practice that was sanctioned by the Federal Housing Administration in the 1930’s with its development of redlined maps that excluded Black and immigrant neighborhoods from receiving mortgage insurance based on the racist underwriting practices of the private insurance industry.[12] In the 1960s, states passed laws to create privately-run[13] insurers of last resort, also called “residual markets,” that explicitly allow insurers to stop individually serving customers in the urban core and instead offer expensive, substandard coverage to these neighborhoods as a consortium.[14] With the advent of these insurers of last resort, private insurers are now able to dump unwanted policyholders and properties onto the last resort plans, which are backstopped by the public in several states. In the 1990s and early 2000s, reports revealed that insurance companies charged higher premiums, provided less comprehensive coverage, offered worse terms, and had lower quality service in Black and Latine neighborhoods.[15] Recent reports reveal ongoing racial discrimination by home insurance companies: Indigenous, Latine, and Black policyholders are disproportionately uninsured,[16] and Black policyholders struggle to get insurers to pay claims.[17]

States must strengthen oversight of insurance rate hikes

Only 15 states currently grant insurance commissioners authority to conduct a review of rate increases and either deny or approve (called “prior approval). In general, state insurance commissioners and legislatures conduct very limited oversight over insurers, and provide little opportunity for public input on insurance rate hikes. The result: few states are standing up to steep price hikes or discriminatory pricing.

Your public official should take public input on local insurance rates

Homeowners, advocates, and the public should have a meaningful opportunity to engage in the insurance rate-setting process to help improve access to affordable insurance. Some states hold hearings on rate-setting and allow people to testify; but most states have no mechanism for public input and hold few public hearings. Individuals are typically not able to initiate a hearing or other formal rate review. Currently, few commissioners appear to take public input into account. The public should be able to provide meaningful input not only into rate-setting but also the racial and economic biases in individual premiums.

California offers the most opportunity for public input. People can formally intervene in the rate review and approval process, attend hearings, submit testimony, and potentially recover the costs of doing so.[18] North Carolina also has limited options for public input: the state insurance department may hold a hearing when rate increases are filed and the public may participate through written or verbal testimony.[19] In some states, insurance commissioners have discretion to hold public rate setting hearings with opportunity for public comment but rarely elect to do so. For example, the Florida Office of Insurance Regulation only held one rate setting hearing in 2025,[20] and the last public hearing they held for the current largest private home insurer in the state (Universal Property and Casualty Insurance Company) was in 2006.[21]

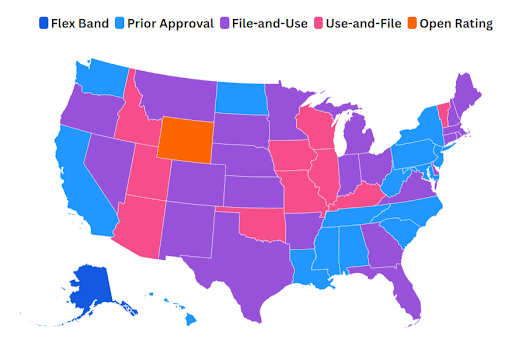

Some states require insurance commissioners to approve rates before they go into effect, while others require the insurance commissioner to intervene to object to proposed rate increases. There are some subtle distinctions but all fall into one of five categories (see map):[22]

- Prior approval (15 states): Insurance commissioners must approve a rate request before it can be implemented. The prior approval process gives the state the ability to negotiate with insurers over rate hikes and can lead to smaller rate increases, as has been shown in auto insurance.[23]

- File-and-use (23 states): Insurers file rates with the state insurance commissioner which has a fixed number of days to review and object, otherwise the insurer can implement the rate. This gives the state the ability to object to rate increases, but states rarely exercise this authority and there is less ability to negotiate over the filed rates.

- Use-and-file (10 states): Insurers simultaneously charge new rates and submit rates to the insurance commissioner. The state can object within a fixed number of days, but otherwise insurers may continue to use the higher rates. This is similar but weaker than file-and-use because it is harder to roll-back premiums that are already being charged. Illinois is technically considered a use-and-file state but the insurance commissioner lacks the authority to even reject requested price increases for homeowners insurance, rather they can only require insurers to adhere to their own rate filings.[24]

- Flex band (Alaska): Insurers file rate requests if the rate increase is below a fixed amount, the application is treated like file-and-use. However, if the rate increase is at or above the threshold, it is considered like prior approval.

- Open rating (Wyoming): Insurers establish rates with a presumption that they comply with state standards. The commission only intervenes in limited circumstances.

State Ratemaking Approval Laws[25]

There are several ways states can and should curb excessive property insurance rate inflation.

Recommendations

Provide Meaningful Review Over Insurance Rate Hikes

- States should pass laws to require insurers to get prior approval for rate hikes from the insurance commissioner. These prior approval ratemaking laws have precedent in several states already, as can be seen in the chart above.

- States should solicit meaningful public input on rate filings—see, for example, California’s public intervenor program and similar programs for utility rates in six states. These measures produce the greatest oversight and negotiating ability over rate increases and can limit disparate racial and economic impacts.

- State insurance departments should maintain a public webpage to describe how the state insurance rate-setting process works in plain language.

- State insurance departments should maintain a public schedule of hearings relating to rate-setting and methods for consumers to participate in the process.

Curb Discriminatory Pricing and Profiteering

- States should ban the use of credit scores to set premiums. This outdated practice has no connection to property-level risk and it perpetuates racial discrimination. Maryland, Massachusetts, and California have already banned the use of credit scores to set insurance premiums through regulation or legislation.

- States should require their insurance regulators to publish the full rate manual for each home insurance carrier in the state, made available to the public to the greatest extent allowable by law, and insurers should be required to file their full up-to-date rate manual with every home insurance rate filing, along with a list of each rate filing over time in which the insurer changed rating rules.

- State insurance departments should closely review and analyze profit margins and administrative costs that insurers propose in their rate filings. Insurance companies with consecutive years of outsized profits should be required to either lower their rates or submit a justification for maintaining their current rates. New York Governor Hochul recently proposed a similar measure.

Provide Discounts and Resources for Climate Resilience

- States should require insurance companies to consider property, community, and landscape-scale climate resilience measures taken by policyholders and communities in their underwriting, and provide policyholders with premium discounts when they take climate resilience measures. States like Alabama, Louisiana, Colorado, and California already have such laws and regulations in place to require or encourage these measures, and some states are also providing grants to households to harden their homes.

Stop the Revolving Door Between Commissioners and the Industry

- States should prohibit insurance commissioners and politically appointed senior staff from taking jobs with the insurance industry when they leave insurance departments.

Download the Report

[1] Property and casualty insurance for residential properties (called “home insurance” or “homeowners insurance”) is regulated at the state level and does not usually include flood coverage or coverage for perils such as earthquakes.

[2] Cornelissen, Sharon et al. Consumer Federation of America “Overburdened: The Dramatic Increase in Homeowners Insurance.” April 2025.

[3] Ibid.

[4] Americans for Financial Reform Education Fund and Public Citizen. “Rising Property Insurance Premiums: The Uneven Risks to Households.” September 18, 2025.

[5] Jones, Dave. The Uninsurable Future: The Climate Threat to Property Insurance

and How to Stop It. Yale Law Journal. December 2025. p. 198.

[6] To view the most recent rate filing from your insurer, check the National Association of Insurance Commissioner’s System for Electronic Rates & Forms Filing (SERFF).

[7] Reinsurance is insurance for insurers; reinsurance premiums paid by insurers to reinsurers are incorporated as an expense in the rate-setting process.

[8] Cornelissen, Sharon et al. Consumer Federation of America. “Overburdened: The Dramatic Increase in Homeowners Insurance.” April 2025.

[9] Jones, Dave. The Uninsurable Future: The Climate Threat to Property Insurance

and How to Stop It. Yale Law Journal. December 2025. p. 198.

[10] Birss, Moira et al. Consumer Federation of America and Climate and Community Institute. “Penalized: The Hidden Cost of Credit Score in Homeowners Insurance Premiums.” August 12, 2025.

[11] Americans for Financial Reform Education Fund and Public Citizen. “Rising Property Insurance Premiums: The Uneven Risks to Households.” September 18, 2025. All but three states allow use of credit scores in calculating home insurance premiums: California, Maryland, and Massachusetts.

[12] Fishback, Price et al. “New Evidence on Redlining by Federal Housing Programs in the 1930s.” Journal of Urban Economics. Vol. 141. May 2024.

[13] Penaranda, Isabel et al. Climate and Community Institute in partnership with Climate Cabinet. “Insurers of Last Resort: Why Today’s FAIR Plans Need a Redesign to Address the Home Insurance Crisis.” October 2025.

[14] Ramzee Nwokolo, “How FAIR Plans Confronted Redlining in America,” Chicago Fed Letter. No. 484. September 2023.

[15] See e.g., Gregory D. Squires. “Insurance Redlining, Still Fact, Not Fiction.” Shelterforce, January 1, 1995; Wissoker, Douglas et al. Urban Institute. “Testing for Discrimination in Home Insurance.” December 1, 1997; Gregory D. Squires. “Racial Profiling, Insurance Style: Insurance Redlining and the Uneven Development of Metropolitan Areas.” Journal of Urban Affairs. Vol. 25. No. 4. 2003; Michael Delong. Consumer Federation of America. “Insurance Contributes to Systemic Racism and Redlining.” June 17, 2022.

[16] Cornelissen, Sharon et al. Consumer Federation of America. “EXPOSED: A Report on 1.6 Trillion Dollars of Uninsured American Homes.” March 12, 2024.

[17] Emily Flitter. “Black Homeowners Struggle to Get Insurers to Pay Claims.” The New York Times. December 29, 2020. Updated January 1, 2021; Emily Flitter. “New Suit Uses Data to Back Racial Bias Claims Against State Farm.” The New York Times. December 14, 2022; Keisha Bross, NAACP, “NAACP Director of Opportunity, Race, and Justice responds to racial bias claims against State Farm.” December 16, 2022.

[18] California Department of Insurance website. “Prop 103 Consumer Intervenor Process.” Accessed November 3, 2025.

[19] See here the statute that governs ratesetting participation requirements in North Carolina.

[20] Florida Office of Insurance Regulation website. Public Hearings. Accessed November 3, 2025.

[21] Florida Office of Insurance Regulation website. Past Public Hearings. Accessed November 3, 2025.

[22] For more information, see the U.S. Department of Treasury Report: “Analyses of U.S. Homeowners Insurance Markets, 2018-2022: Climate-Related Risks and Other Factors,” January 2025.

[23] J. Robert Hunter, Tom Feltner, and Douglas Heller. “What Works: A Review of Auto Insurance Rate Regulation in America and How Best Practices Save Billions of Dollars.” November 2013.

[24] Peter Hancock, “Pritzker seeks more regulatory authority over homeowners insurance business.” Capitol News Illinois. July 17, 2025.

[25] For more information, see the U.S. Department of Treasury Report: “Analyses of U.S. Homeowners Insurance Markets, 2018-2022: Climate-Related Risks and Other Factors,” January 2025.